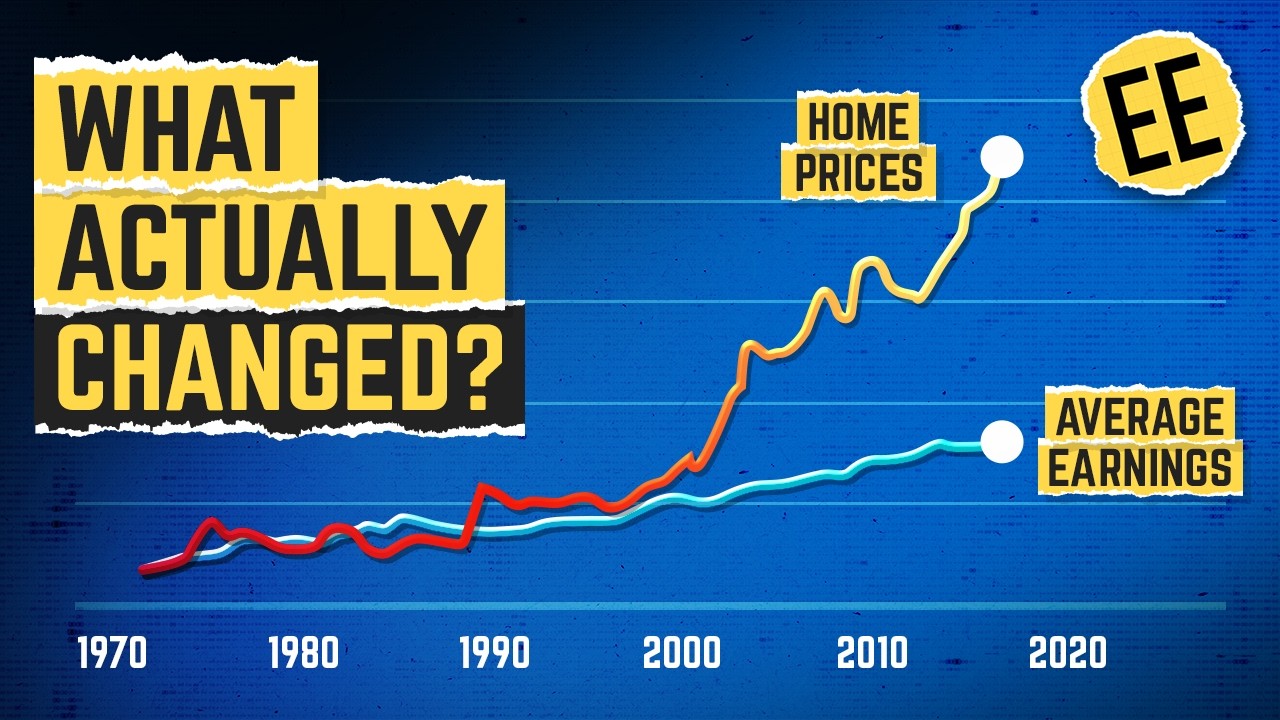

For most of the 20th century, a typical house cost about 3 times the typical households income. People could buy a place with 3 years of pay and that used to be normal. But of course, it's changed. A global study looked at 95 major cities and found that not a single one is considered affordable anymore. Even the so called normal cities have slipped out of reach. Across these centres, the average home now costs more than 5 times what a typical household earns and in places like Hong Kong, Sydney and Vancouver, that number isn't 5, it's 9, 10, even 14 times income. And they aren't even the worst. In Beijing and Shanghai, price to income ratios routinely exceed 20 or even 30 times, showing just how far the gap can stretch in the world's most pressured markets. So yes, it's official. The dream of owning a home is dying, not in one country, but in all of them. And when that dream disappears, a lot of other things start disappearing with it. As homes turn into investment opportunities instead of places to live, people put off having kids because they can't afford the space, they turn down better jobs because moving costs too much, and younger generations stop saving altogether, because what's the point of saving for something that you'll never be able to afford anyway? The result of this shift is a strange economy where the people who build our cities teach our kids and keep everything running can't afford to live in the very places they keep alive. So how did we get into this mess? If people can't afford to populate these cities, can prices really get any worse? And finally, what would it actually take to fix it? Have you ever started writing an email to a client or colleague and just not known where to begin? Between scripting, emailing and going back and forth with collaborators, writing is all I do, and getting started can be the most challenging part. That's why I use Grammarly. It's an AI writing partner that helps professionals with all their writing needs from start to finish, providing personalised suggestions that sound like you. I've been using their AI chat to help me get past my writer's block and straight into writing. It also has a humaniser tool that helps your writing sound more natural by adding warmth and making your words more natural, but on top of that it can examine your writing and provide topic specific feedback with its expert review feature which uses feedback inspired by experts in the field to help elevate your writing. Another cool thing is how you can download Grammarly on your phone and send those last-minute emails to your team on the go. If you want to improve your writing and ideation, whether it's for work, side projects or just for clearer communication, sign up and upgrade to Grammarly Pro to level up your productivity. You can use my link for 20% off-pro. Thanks again to Grammarly for sponsoring this video. Every year, Chapman University releases the Demografia International Housing Affordability Report, one of the most detailed looks at living costs anywhere. It compares house prices to household incomes across 95 cities like Sydney, Toronto, London and San Francisco, and it shows where the dream of home ownership still exists and where it's completely gone. Researchers use something called the Median Multiple, the price of a typical home divided by a typical household's yearly income. In a healthy market, that number sits around three, but this year something unprecedented happened. For the first time in the report's 21-year history, not a single market was considered affordable. While conditions vary, most of the 95 cities now fall into the seriously or severely unaffordable categories, meaning a typical home costs more than four to five times what a typical household earns. And in 12 of them, things have gotten so bad, they added a new label. Impossibly unaffordable, where the median home costs more than nine times the median income. At the top of this list is Hong Kong at 14. 4 times income, and Sydney isn't far behind at 13. 8. Then comes San Jose, Vancouver and Los Angeles. And once you start looking beyond those cities, you realise the same pattern repeats across entire countries. Homes in Australia's average city are now near 10 times median income, even small markets like Perth or Brisbane are now less affordable than New York. In Canada, affordability has been collapsing since the mid-2000s. Vancouver has ranked amongst the fourth least affordable cities on earth for 18 years straight, and Toronto isn't far behind. Greater London homes now sit at nine times median income, while the UK average has crept to 5. 6, which is roughly double what it was in the 1990s. Even the United States, one known for its sprawling suburbs and cheaper housing, has climbed from 3. 9 before the pandemic to 4. 8 today. For context, Pittsburgh, the most affordable city on the list, sits at 3. 2. That used to be normal, now it's a miracle. Just 30 years ago, nearly all these cities were affordable. Home prices rose roughly in line with incomes, but today they've completely split apart. The report's authors call this an existential threat to middle income households, and you don't need to be a researcher to see why. When home prices rise faster than wages, the effects spread far beyond the housing market. Families delay having kids, workers turn down better jobs because they can't afford to move, and younger generations lose access to what used to be the cornerstone of middle class life, owning a home. Which raises the bigger question, if this wasn't a problem 30 years ago, what changed? 30 years ago, a house was a shelter, it was a basic need. Today, it's part of a global investment strategy, but this isn't just about housing. Over the last few

Segment 2 (05:00 - 10:00)

decades, almost everything that counts as an asset has shot up in price. Not just homes, but land, stocks and even art. Why? Because rich people, corporations and big funds have more cash than ever, and they all want a safe place to park it. When the wealthy get more money, they don't buy more groceries. They buy assets. Housing got hit the hardest because it's both essential and one of the easiest assets to own, rent out or borrow against. It became the perfect target. This artificially boosted demand, while at the same time we were arbitrarily limiting supply. It began with good intentions, protecting green space, controlling sprawl, preserving neighborhood character, but over time, those good intentions turned into zoning limits, height caps, parking minimums, endless approvals, all of which slow construction and drove up the cost of land that could be developed. As those restrictions tightened, housing stopped behaving like a normal market. Prices no longer reflected the cost of bricks and labour, they reflected policy-made scarcity. As interest rates fell and global cash supplies surged, more capital chased the same limited number of homes. Investors, funds and even pension systems realised that real estate offered steady returns and safety from inflation. If you could borrow at 3%, your property rose 7% a year, you didn't need to live in it, you just needed to own it. This shift turned homes into financial products, institutional buyers started purchasing single-family homes in bulk, foreign investors traded a property as a storehouse of wealth, and even regular households began to see real estate as something that always went up. That wave of money flowed straight into the cities already at the top of Demografia's list, where limited supply sent prices through the roof. In markets like these, the more valuable housing became, the more capital attracted, creating a feedback loop between scarcity and speculation. Meanwhile, wages stopped keeping up. For most of the 20th century, income and house prices moved together. As workers became more productive, they earned more, and as cities grew, they added more homes. But in the 1990s, those trajectories diverged. Trade, automation and offshoring put a lid on middle-income wage growth, even as living costs rose. In the US, median real wages have risen only around 10% in the last 20 years, while home prices have doubled, tripled or even quadrupled in the same period. A few decades ago, a single income could buy a family home, and if a second earner joined the workforce, that meant a bigger house or a better neighbourhood. But once everyone had two incomes, sellers knew it and prices climbed to keep pace. Instead of making homes more affordable, dual incomes just made the same homes cost twice as much. And as prices rose faster than pay, something else happened. People stretched further into debt. People would end up spending more of their income on a mortgage, banks would keep lending because rising prices made the market look safe, and every time lenders approved bigger loans, buyers could bid higher, pushing prices up again. It created a feedback loop that kept feeding itself. But then the pandemic hit and the whole system started to wobble. Remote work scattered demand into smaller cities, but it didn't fix the core problem. Construction costs exploded, supply chains broke, inflation sent material prices soaring, and labour shortages slowed projects everywhere. When interest rates finally rose, borrowing got expensive, but prices didn't crash because nobody wanted to sell. Millions of homeowners were locked into ultra-low-rate mortgages and refused to move, so supply froze. Governments tried to help, but mostly in the wrong way. They rolled out even more tax breaks, grants and subsidies to first home buyers. The problem is that when you can't build more homes, giving people more money doesn't make prices fall, it just makes buyers fight harder over the same ones. So, if you trace it back, the answer to what changed isn't one thing, it's a chain reaction. We restricted land, we flooded the system with cheap money, we let wages stagnate while asset prices took off, and when the foundations of that whole system started to crack, we doubled down with short-term fixes, piling bricks on top and just hoping gravity would take the day off. That's how we ended up with impossibly unaffordable places to live, and why today, the world's richest cities now top the list of the least affordable places on earth. So, what does that actually mean for the people living in them? For millions of middle-income families, it means home ownership is no longer part of the plan. In cities like Los Angeles, Sydney and New York, a large share of renters now spend about 30 to 35% of their income just keeping a roof over their heads, right above the threshold economists unaffordable. The average first-time home buyer is now in their late 30s or early 40s, a full decade older than their parents were, and when the people can't afford to live where their jobs are, they stop moving for opportunity. In the US and Canada, people are leaving major cities for small towns, a trend economists call counter-rebonisation. And while that might sound like a good thing for regional growth, it often means the most productive cities lose the very workers that keep them running, teachers, nurses, tradespeople, hospitality staff. A locked housing market becomes a locked labour market. Productivity slows, innovation spreads more slowly, and inequality deepens. Because while renters and first-time home buyers are falling behind, existing homeowners keep getting richer. Every year their homes gain value, not because they worked more hours or invented something new, but because scarcity made their property worth more. Globally, the total value of real estate now sits at around three and a half times the world's annual GDP. And even for people who are lucky enough to grab onto the ladder, buying in at such elevated

Segment 3 (10:00 - 12:00)

prices feels like a gamble, high debt, high risk, and the constant fear that one economic shock could knock everything off balance. So, is there any way to stop this? Some countries are starting to try. New Zealand launched a plan called Going for Housing Growth in 2023, which forces major city councils to zone enough land for 30 years of housing demand. Their goal is simple – make land supply predictable so prices can't spiral out of control. In the US, cities like Minneapolis and states like California have begun loosening single-family zoning. That means duplexes and small apartment blocks can be built in neighborhoods that once allowed only one house per lot. This opens up supply where people actually want to live. Singapore is taking a completely different approach. There, nearly 90% of households own their homes thanks to massive public housing program managed by the Housing and Development Board. The government buys land, builds at scale, and sells apartments directly to citizens at subsidized prices. So yes, this shows that if you treat housing as infrastructure, like roads or schools, you can achieve near-universal ownership. Then there are countries tackling speculation instead of supply. Hong Kong and Wales both tax second homes heavily. In Wales, local councils can charge up to 300% council tax premium. Taiwan packs its property sold within two years at up to 45%, discouraging fast flips and speculative buying. And in the Netherlands, some municipalities have banned investors from buying in certain neighborhoods to keep homes for locals. The US is now exploring a similar idea with the End Hedge Fund Control of American Homes Act. This act would stop hedge funds and other big real estate firms from owning single-family homes altogether. So yes, to fix this crisis, we need more homes. But we also need to rethink who's buying them, where they're built, and what kind of economy they're fueling. Because at its core, it's the same old story. A tidal wave of money flowing into a handful of assets and drowning the middle and low-income classes in the process. And unless certain balance changes, no amount of zoning reform or new construction will make homes truly affordable. If you want to understand why inequality is now reaching a tipping point and how we got here, we've already made an entire video on that exact topic and you should be able to click that on your screen now. Thanks for watching mate, bye.