Live Q&A where we dive deep into the latest student loan news, upcoming deadlines, and strategies to maximize your loan forgiveness. In this session, we cover everything from the growing PSLF buyback backlog and navigating repayment plan transitions, to the critical June 30th consolidation deadline for Parent PLUS borrowers.

Whether you're a parent figuring out how to pay for your child's college, a public servant tracking your 120 qualifying payments, or someone navigating repayment during unemployment or disability, this stream is packed with actionable advice. Check out the timestamps below to jump straight to the questions and topics that matter most to your financial situation!

Timestamps:

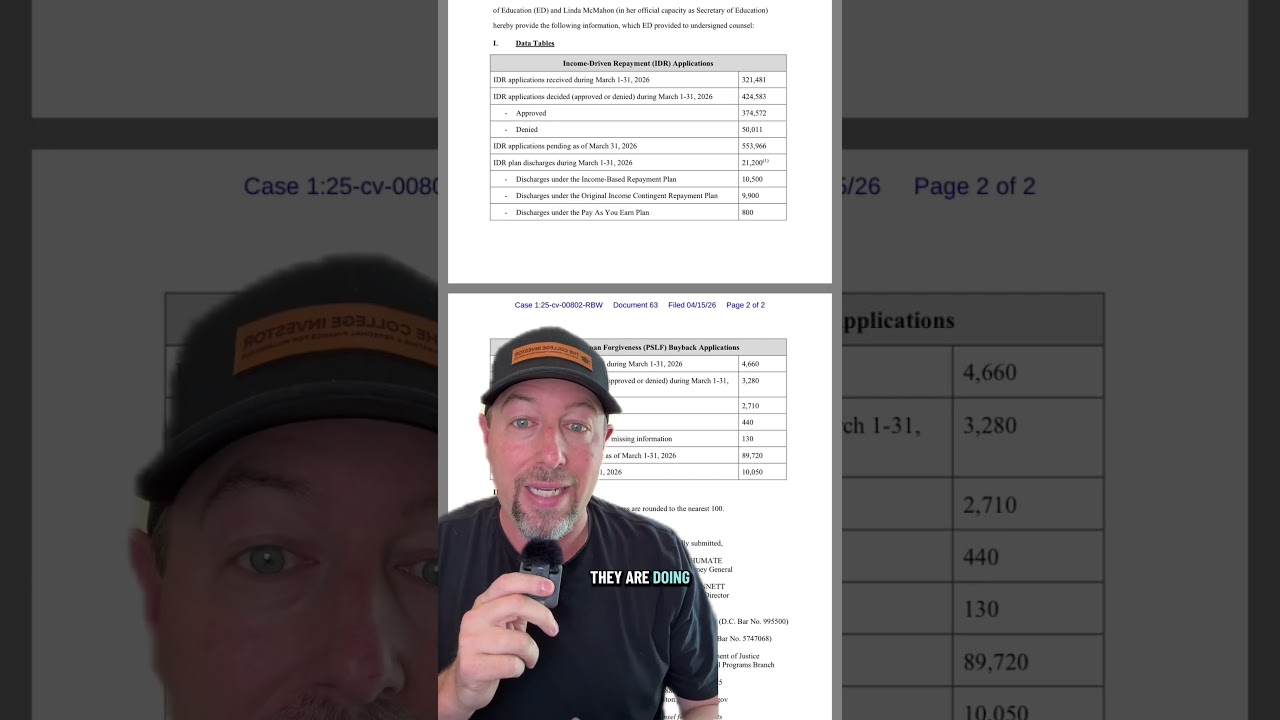

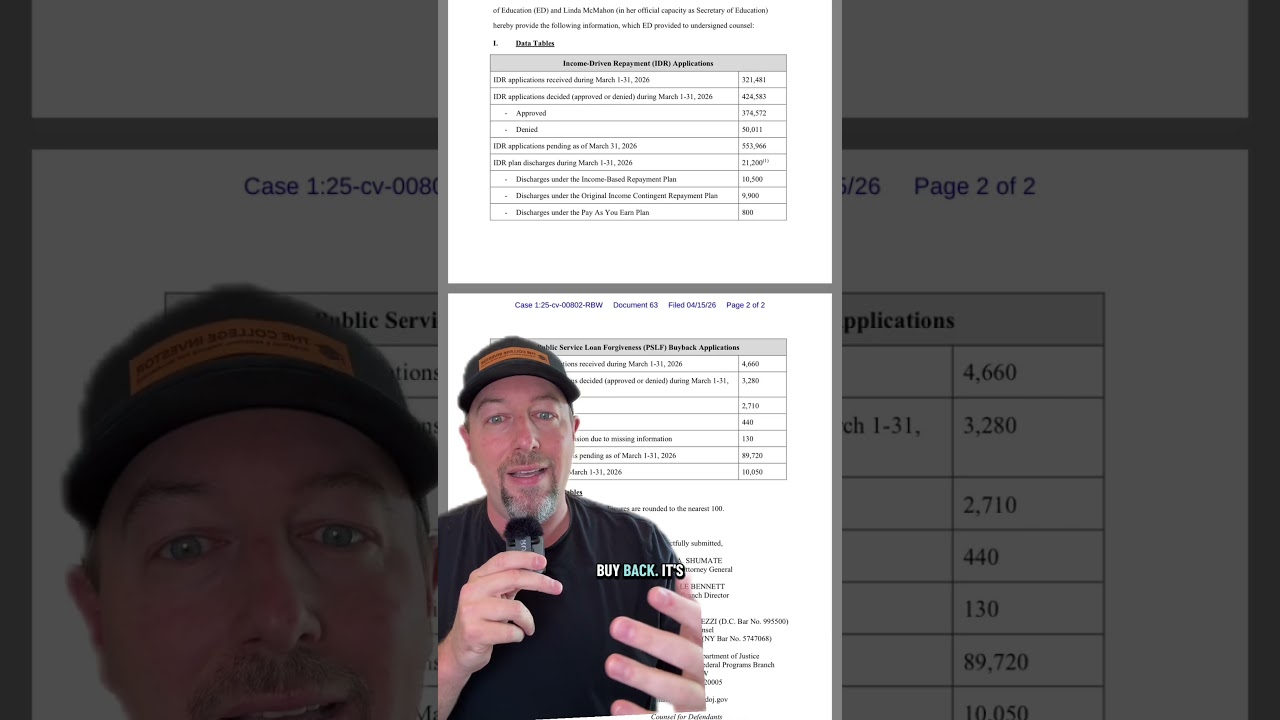

00:00 - Welcome & PSLF Buyback Backlog Updates

02:40 - Order of Operations: Federal vs. Private Student Loans

05:15 - Parent PLUS Loans: Why You Must Consolidate Before the Deadline

09:30 - How Married Filing Separately Impacts Income-Driven Repayment

14:20 - Is a College Degree Worth the Debt? (The $80k Limit)

19:45 - How to Hack Repayment if You Move Abroad (Foreign Earned Income)

24:10 - Public Service Loan Forgiveness (PSLF) for Nurses & Teachers Explained

33:00 - Using Alternative Documentation for Job Loss or Income Drops

41:20 - Should You Empty a 529 Plan Before Taking Out Loans?

52:10 - Do In-School Deferment Payments Count Toward PSLF?

1:05:00 - FAFSA Appeals & Negotiating Financial Aid

1:15:30 - Securing $0 Monthly Payments if Unemployed or Disabled

1:28:40 - Standard Repayment vs. IDR for Paying Off Debt Fast

1:42:15 - High School Prep: Why Middle School Math Impacts Merit Aid

1:51:50 - Warning: Avoid Variable Life Insurance Products

1:55:00 - Lightning Round Q&A & Final Thoughts

Оглавление (16 сегментов)

Welcome & PSLF Buyback Backlog Updates

All right, let's get this show on the road. Welcome, welcome, guys. We are just getting started with this week's live Q& A. Uh, it's been a couple weeks, so I'm excited to get this started. If you guys have any questions, you guys know the deal. Drop them in the chat. We'll also uh invite people up on stage. If you want to come up on stage, just let me know and we can talk. And uh yeah, we'll get this thing going. Pardon the housekeeping while I get this shared out. Welcome, guys. I love seeing everyone popping in here. Hello. We're starting to get some folks trickling in. I love it. I love seeing y'all here. All right, let's get this set up because like I feel like it's been two weeks so I have lost my setup. Welcome, guys. All right, now we are getting some folks in here. Oh, welcome Eleanor and Alex and Nurse Truly and Margaret and Reie. Peace, love. Getting some folks in here. I love seeing that. So, uh, welcome guys if you're just joining us. My name is Robert. I'm the founder of The College Investor and you guys know that we talk about money and education here on the channel. Hey, thank you very much. Always appreciate the gift, Elizabeth. That is lovely. We are going to do a nice little live Q& A for a little bit. Uh if you are just joining us, feel free to drop your question in the chat or shoot me a message and I'll invite you up as a guest if you want to speak your questions. I know it's been a couple weeks. I hope uh everyone had a nice spring break. I did. Um, and so now we are back in the grind of things and uh

Order of Operations: Federal vs. Private Student Loans

yeah, we had some news today with the PSLF buyback and the R processing backlog and uh, I feel like there's been a lot of other news lately and I'm sure I'm forgetting stuff, but if you guys have questions about it, how it applies to you, what you're thinking about, drop it in the chat and we will discuss it or come on up. Welcome Joanne and Alexa. Appreciate you being here. And Holden, welcome. Corey, what happened with buyback? Well, we got the latest numbers, Elizabeth. Um, so, you know, every month on the 15th, they report the latest numbers. It's actually my last video, too, if you want to watch it. But, uh, basically the backlog got bigger. They processed more applications. So technically if you know are in the buyback line it's about 27 months now instead of 35 months. So still over two years and again like I'm reiterating the number of denials are rising. Uh, and I expect that to continue because I think a lot of people are going to end up hitting PSLF the normal way. Um, well before they get their buybacks processed, right? Because most people are trying to buy back save. They're maybe 8 to 12, maybe 15 months of payments, maybe a little more, but 15 months versus 27 months, you're going to finish normal PSLF well before your buyback application is processed. And uh that's why the denials are growing because that's what's happening to people, right? They were waiting for their buyback. They hopped on to IBR, finished it. Tyler, thoughts on doctor's loans? So doctors should always borrow in the order of operations, right? Federal loans first up to your limit and then you supplement with private student loans. Uh honestly, that's the way you do it. There's not much to it. You just go shop around, get three to five quotes on the private loans and rock and roll. Alexa, is it possible to get refinancing without a co-signer with a credit score of 700? It is possible. I would encourage you to shop around and see if anyone's going to offer you any options. Um, I think don't focus so much on the credit score, though. It's going to be the income that's real deciding factor for you, Alexa. And so, they don't just want to see good credit. You have you okay credit, uh, but they're going to want to see enough income to have a good debt to income ratio on whatever it is that your

Parent PLUS Loans: Why You Must Consolidate Before the Deadline

loan balance is. Joanne, parent plus loan consolidated, awaiting for ICR, one payment then to I guess you mean IBR. Um, yep. So once you consolidate, you make your one ICR payment, you wait for the billing cycle to end and then you can apply for IBR. Uh Joanne, uh, you can always file your taxes married filing separately. There's no new law, old law, there's no changes. The same rules have always applied. File separately. It uses your income. File jointly. It uses your joint income. All right. Uh Dina, I just filed my 2025 taxes. How soon can I use these for my new claimment? What's the process? Uh as soon as your tax returns processed, it's going to pull it automatically and you just apply on studentaid. gov and it will go from there. Jay, I'm paying off my loans. 5x the minimum. Um great job. No, no mus or fuss with that one. Uh, Angelica, my daughter got a full ride but still has the student portion to pay and it's high. Yeah. So, all these student responsibility, I don't know what high is. Uh, most student responsibility I see is like 2,000 5,000 bucks. That's really not high. Um, so you just have to ask yourself how you going to pay it. You can borrow. I encourage your child to work. So, most of those student responsibility amounts are very doable with work, right? Um, $2,000 a year, $5,000 a year. You could easily earn that just working at a coffee shop. So, that's where that comes from. And something to think about. You can do it with a payment plan, too. Uh, Cynthia, I'm on save. I just did my taxes filed separate. What's the best time to switch to IBR? As soon as it's processed. So, I don't know when you filed. Did you file? I mean, today is the tax filing deadline, so I'm going to assume that everyone's already filed or filed today. Um, the biggest thing is just make sure it's processed and then go from there. Um, best advice for college student who didn't get any financial aid but still wants to attend. Sassy, the big thing is, uh, pick a college that you can afford. If you didn't get any financial aid, it usually means your parents also have a lot of money. And so I don't know if they're helping you, not helping you, all the different things what that looks like, but pick a college you can afford. If you saw my video from like 3 days ago, it just keeps reiterating the same point over and over again, and I've said it for a couple years now. The maximum value of a bachelor's degree is $80,000. That's it. So spend less than that, borrow less than that, you'll be okay. Spend more than that, you're going to get yourself into financial trouble. Um, Crystal Ball, why did I only find out about compounding interest at 49? Am I cooked? Uh, it cuts both ways, Crystal Ball. So, you're not cooked because compound interest works to help you. It hurt. Well, it can hurt you, too. So, get out of debt, start saving and investing, and start rocking and rolling. How big is my roll of quarters? I haven't had a roll of quarters in ages. Uh I think random I think random's actually uh asking inappropriate things. All right, here we go. Did you know do you know there is a forgiveness program? Marina, there Miranda, there are 80 plus ways to get student loan forgiveness. The most popular ones are public service loan forgiveness, teacher loan forgiveness, timebased loan forgiveness because of your repayment plan. You got death and disability. You got 80 different or 48 states have their own different state programs. There's so many options out there. Lisa, what do I do if it's hard for me to pay my student loans and find a higher paying job? Lisa, well, first off, make sure you're on the correct repayment plan for your student loans. So, the lowest options for you today are going to be IBR. Coming up this summer is going to be the RA plan. IBR caps your monthly payment at 10% or 15%, 10% if your first loan was after 2014. So, what are you doing with the other 90% of your actually going to be like 95% of your money? Um, it would be the first question. So, it's a tough spot to be

How Married Filing Separately Impacts Income-Driven Repayment

in, but make sure you're in the right repayment plan. And also make sure you are certified for your current income. Like, did you miss a certification? Is it reflective of your current income? Do you need to update it because you got a new job, a lower paying job? Make sure it's up todate. Hey guys, we have over 50 of you in here. I love it. Make sure you throw some hearts down on that screen to tell Tik Tok that we're live because that goes a long way. Part two is if you're not following us here at the college investor, please do. We talk about the intersection of money and education, right? So that's student loans, financial aid, saving for college, paying for college. We talk a lot about financial literacy um because it all goes handinand. If that stuff is important to you and you want good, accurate advice, this is what we do. We've been doing this since 2009. We are not just Tik Tok creators that popped up on here. We actually have a whole team. Some of them have been doing this 20, 30 years longer than I have. And this is what we do. So, please like, subscribe, and follow if that is important to you. And uh I love to use this time to take the news in the big picture and help answer these nuanced questions um that you guys are dropping in the chat. And I love seeing it. So, thank you guys for the likes and the follows. Lindsay asks, "For a parent plus loan, do you recommend one payment on ICR and then do and I think you mean IBR? " B is in boy cuz it's income based repayment, Lindsay. And yes, absolutely. Income based repayment will give you a lower monthly payment than income contingent repayment. So, do your one ICR payment, finish the billing cycle, and then apply for IBR. Uh, Victoria says, "How soon before the 120th payment should I submit for forgiveness and apply for buyback? " Uh, Victoria, you cannot apply for buyback until you've crossed the 120. Not before, crossed it. And so, honestly, for you, if for you, buyback's going to be moot, Victoria. I wouldn't even consider doing buyback. Now, it doesn't hurt to put the application in if like by some miracle they eliminate a 27 plus month backlog and get caught up, but honestly, Victoria, just plan on doing PSLF the normal way. Um, you're probably going to be not buying back. Got into Michigan Ross 70k or humorous ammeris 25k. Uh, I don't know your name. Dot. I'm going to call you dot. Always the cheaper school. There is no difference. I was actually at a education conference all the last few days and uh I was sitting in a room with the Gallup um foundation and they do all those polls, right? And one of the interesting things they did was they pulled Fortune 500 employers and one of the questions they asked them was does where you went to college or does where applicants go to college matter to you at all? And literally if you go to a top 200 school in America, it's exactly the same. There is no difference to an employer where you went to school. And so no difference dot just do the cheapest possible school that you can do, especially for just like a business degree. Um Jay Jimenez, I didn't get approved for FAFSA this year. Uh, I don't know if you applied. It's not really like an approved or denied. It's you fill out the FAFSA, they give you an SAI number, and the SAI number determines what types of financial aid you're available for. The FAFSA is just a application, federal free application for federal financial aid, federal student aid. Um, Laura, how can my save plan say the next thing I do is 2028 and then make me switch to a new plan in two months? Because like we've said for a year and a half now, Laura, that date is a placeholder date. It's not your actual date. Part two is if you go watch uh our friend Jay, the student loan lawyer, he made a great video on this on why they chose that date because inside the antiquated Excel spreadsheet that is our student loan system, they had to put a date in there and they had to pick one that they wouldn't have to keep updating every single month. And so that's why they picked that date. With that being said, how can they change it for you? Well, Congress passed a law and then the save rules that weren't laws. They were just executive orders got shot down by the courts. And so you had two things working against you. And Laura, I'm sad to say that you're going to have to choose a new repayment plan. And we've been telling you this for a year. Someone yelled at me and said, "Oh my god, Robert, you're finally right. " And

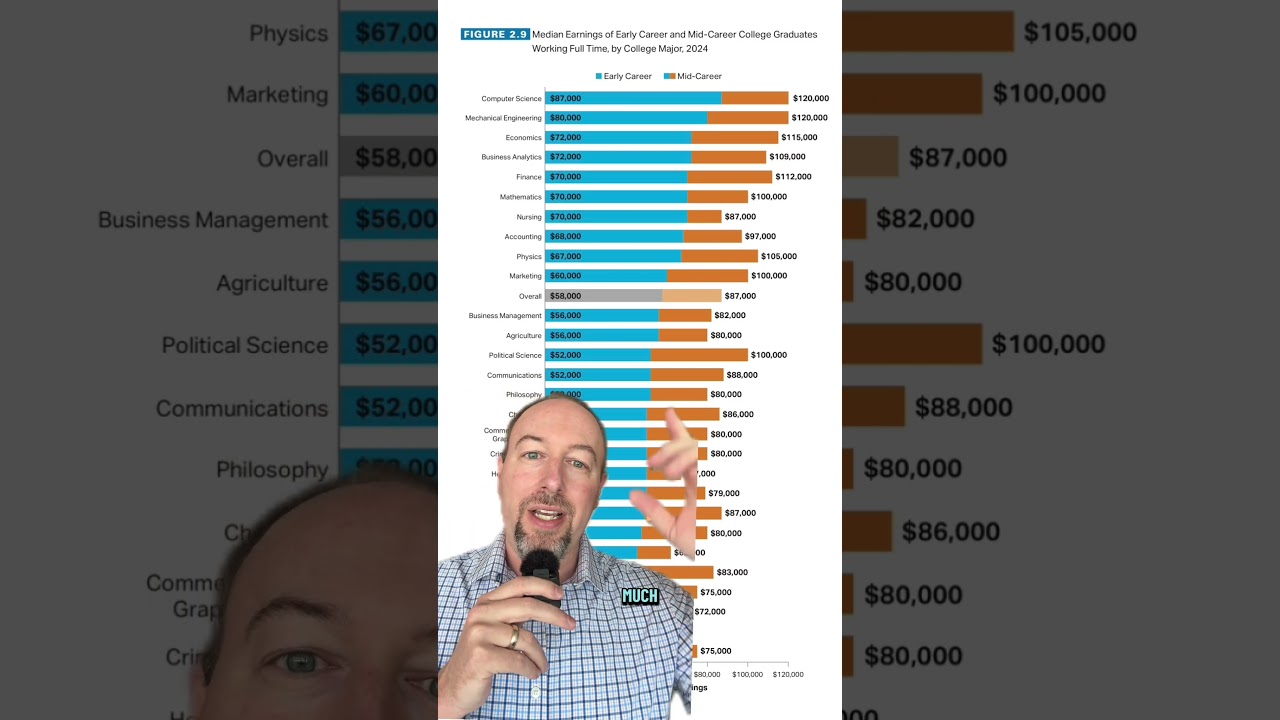

Is a College Degree Worth the Debt? (The $80k Limit)

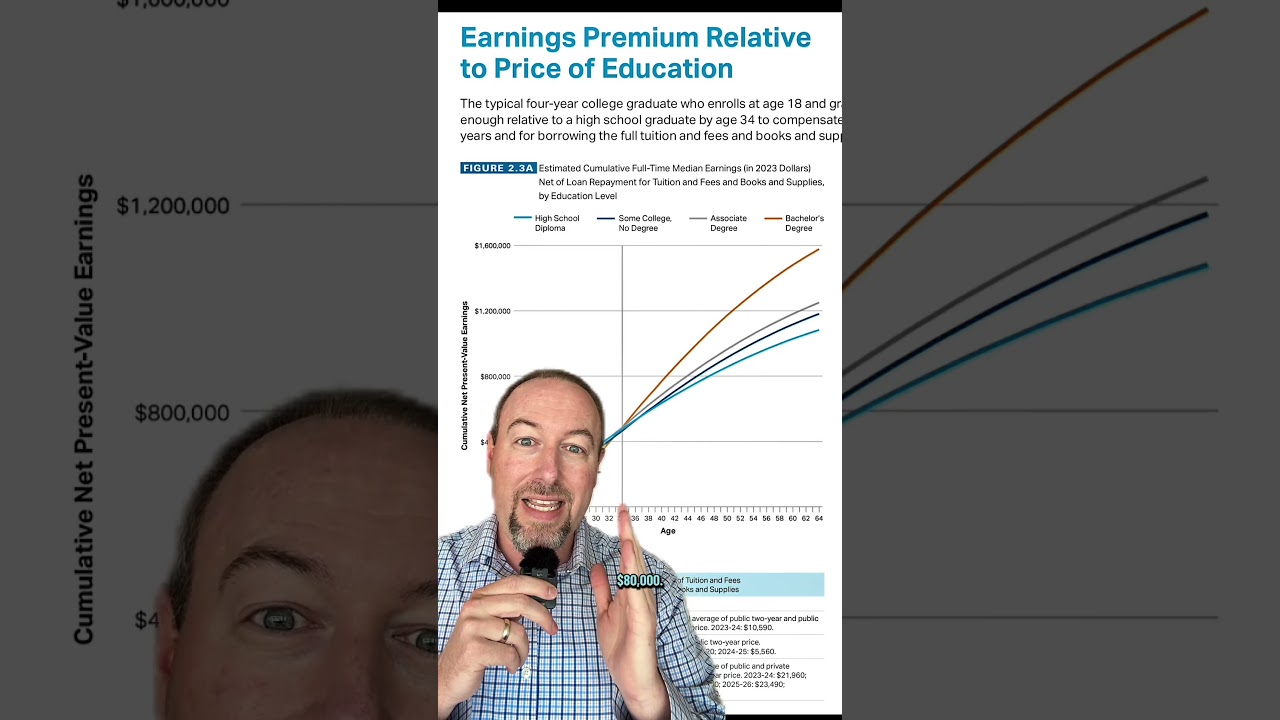

I was like, "Sorry, it took me a I couldn't get the exact time right, but we were pretty darn close. " Um, Derek, looking for companies that offer subsidized loans. So, subsidized loans are only offered by the federal government. You apply for the FAFSA, you get approved. The most you're going to get in subsidized loans is $3,500 as a freshman. I think it's $4,500 as a sophomore and $5,500 a junior senior. And that's it. And then anything else is going to be unsubsidized up to the total amount 5500 6500 7500 and then of course anything that's private definitely not subsidized. Um Crystal moving to Germany do I need to pay my student loans? Absolutely you do. But Crystal, if you didn't watch my video from like last week, uh I talk about how you can hack moving to Germany to make your student loans zero or very little. And it's because you can have the foreign income exclusion tax credit. So up to like I want to say it's $130,000 this year of foreign income you get to deduct from your taxes. So you could have a big fat zero on your American tax return. And guess what? You could use that zero on your US tax return to certify your student loan payments and now are zero. So go watch the video, Crystal. Uh, it's a great way to take advantage of the fact that you're living and working overseas. Um, can I buy back months that I was working for a qualified employer but doing my masters? T- MC, you can buy back undergraduate loans that went into inschool deferment because of your masters. Yes, you cannot buy back the loans you took out for said masters while you were getting said masters. There's a difference in classification for inschool deferment and inschool status for the loans. So your old undergraduate loans that you might have had that went into inschool deferment. Yes. The ones that you took out for the masters if any. No. RH says when you consolidate your in ICR your parent plus loans well the new balance and the loan interest um I don't know what the loan interest the same as standard but when you consolidate your parent plus loans uh your new loan will have the weighted average of all your underlying loans. So mathematically the new loan will be mathematically identical. With that being said, uh there are some nuances like if you were on an autopay discount, your new loan won't have the autopay discount until you enroll in autopay. Things like that. Daisy, what's the deal with interest acrewing while I'm on IBR? Interest always acrru loans. Uh Daisy, so don't really know the question on that one. Maybe that was a new thing though for you that you didn't know that. Mama, uh, I haven't had her in three payments on 195,000. I have two parent plus loans at 15 at zero pay. Mama, should I consolidate? I don't quite know your question, but the question of should you consolidate your parent plus loans is if you need access to IBR and public service loan forgiveness, you need to consolidate today. If you don't care about having access to income driven repayment for your parent plus loans, you don't have to consolidate. Bulldog nurse, how does someone get out of student loans besides paying them off? Bulldog nurse. Great question. So about 50% of borrowers qualify for loan forgiveness programs. You're a nurse. So assuming that you work in public service, so you work for a hospital, a nonprofit clinic, a nonprofit health care group like Kaiser, anything like that will qualify your employment to qualify you for public service loan forgiveness. It's the best program out there because you work for 10 years, you make payments on an income driven repayment plan for 10 years, and any remaining balance is forgiven from your student loans. And so that's the way a lot of doctors, nurses, and health care professionals get student loan forgiveness. The other secondary benefit is because you're on an income driven repayment plan for those 10 years, it's the lowest monthly payment you're going to have. And there's also levers you can pull to hack it, right? You can contribute more to your 403b and you can contribute to an HSA and contribute to a traditional IRA. And you can lower your taxable income by saving and investing for yourself. and that brings down your adjusted gross income. It also will lower your eventual student loan payment. So, that's how a lot of nurses do it, Bulldog Nurse. Um, something to think about. And if you don't work for a nonprofit healthcare provider, well, then it is just going to be paying it off. Tom Collins, uh, I have a parent plus loan for my son, but he has a year left and payments are deferred. Do we do anything now? So, Tom Collins, same exact question or same exact answer. If you need access to income driven repayment and public service loan forgiveness, you have to consolidate, but you also can't borrow again a parent plus loan. You can borrow privately. But then I would also challenge you if you can't afford the payments you have now on standard. What are you going to do for paying for next year? You're in a very tough situation. I made a video

How to Hack Repayment if You Move Abroad (Foreign Earned Income)

about this and none of the options are that great for you, Tom. Um, you're just going to have to kind of work through which one makes the most sense for you. Uh, Lindsay, I don't know why, but they put me for $0 payment for one year. Lindsay, if you're low income and your actual payment is $0, that is a PSLF eligible payment. If you're in deferment or forbearance, not PSLF eligible. So, there's a lot of borrowers, about 20% or so of all the Save Plan, IBR plan borrowers get a Z payment because they're low income. And that is a legal payment. You can just roll with that. Hey, big game. Welcome. Uh, do you think the tax bomb will be resolved eventually? I got a few coming up in a few years. Honestly, I think, you know, we have our tax bomb calculator. It's generally overblown. I don't know if it will be in your situation. Um, I don't know. I really don't know. I actually think it's a very easy one for them to legislate away because it doesn't make a lot of money for the government and it's kind of tedious, right? So, I could see it as an easy win for them to um get rid of the tax bomb, make student loans always uh tax-free forgiveness. With that being said, though, when they do those type of gimmies, they usually get you somewhere else. So, who knows? K Villains says, "When do we know we have to switch? I haven't got an email from Advantage. " So, the first well, first off, if you haven't gotten an email yet, K Villains, go online, make sure your contact information is updated, your email address is correct, phone number is on there, address is good. Um, with that being said, this one was just like I call it the friendly warning notice, and then July 1st is when they're going to put down the hammer of like get out. Um, it's April 15th, man. I don't know if you should go now or later. I you kind of missed the window to take advantage of lowering your payments unless you didn't file a tax return this year. So, K villains, I guess I'd ask you if you have a lower income today than your tax returns, you want to use the alternative method, uh you're unemployed, something like that, switch today. Take advantage of it. Lower your payments. Otherwise, you got a couple months. Um you got to do it by September 30th, though. And don't wait till the end, dude. end. My goodness. Do it in July or August. Uh Duncan Dempsey says, "Would you recommend paying off your student loans as fast as you can, even if it means living uncomfortably? " Duncan, if you are one of the 50% of student loan borrowers that is getting no type of student loan forgiveness, then absolutely get out of debt as quick as because you can. There's an asterisk to that though. Don't do it at the expense of 401k matching contributions. HSA matching contributions. You don't pass up free money to get off your get your student loans paid off. So, always do enough to get any free money you're eligible for and then yeah, throw the rest at it. And living uncomfortable. Absolutely. I'd rather live uncomfortable when I'm 22, 25, 28 than living uncomfortable at 38 and 40. So, yeah. Danielle, what to do if your parents file for bankruptcy and child's going into one year of school, first year of school? What do you do for the loan options? That's going to be a tough one, Danielle, because um as you know, they're not going to be parent plus loan eligible. They're probably not going to be private loan eligible. So, the student can borrow their 5500 in their own name. And I would be looking at very inexpensive schooling options. So, I would look at community college that might be free in your state. I would be looking at online schools, University of the People, ASU online. I would look for employers that pay for a college education. Go work at Chick-fil-A, Target, Walmart, Starbucks, whatever. Um, get to work, get a free education, transfer later if financial circumstances change, but there are still a lot of paths to a very lowcost or free bachelor's degree. Cindy, I haven't touched my student loans in 8 years. Uh Cindy, now's the time to log in and look and make sure

Public Service Loan Forgiveness (PSLF) for Nurses & Teachers Explained

you know what is happening. One of the big things with collections moving to the Department of the Treasury is they're not going to dick around pretty soon. They are going to start coming after you on all four cylinders, six cylinders, eight cylinders, whatever car we're driving. They're going to come after you. And there is no statute of limitations on federal student loans. And so you might have slipped through the cracks with the COVID forbearance and the save plan forbearance and all the other things. And uh those are going to be filled in pretty quick, especially with all the automation these days and AI and all the things. For a parent plus loan, can they come after me if the parent doesn't pay them? Alyssa, no. Parent plus loans are 100% your parents responsibility. You have no legal obligation to them. Uh f off Tik Tok says, "Should I apply for buyback even though I don't have 120 payments? " You can't. It'll get your application denied. Don't do it. It's literally one of the other biggest reasons for denials is that people apply before 120. Perhaps not. Says, "I went back to school for my NBA. Are unsubsidized loans my best bet? " So, you only get unsubsidized graduate loans? Uh, your question, I think, is really federal loans or private loans. And yes, always borrow your federal student loans first and then supplement with private. And perhaps not. Please, please be very careful. I really don't like seeing people self-fund an MBA. Uh MBAs are probably the riskiest financial master's degree out there. 50% of them are negative ROIs. 40% of them are break even. only 10% of them have like above average financial returns. So, I'll be very careful on that one. Perhaps not. Uh, Freddy, is it smart to do a lump sum to pay off the interest so I can start paying the principal ASAP? Freddy, if that's your goal to pay off your student loans, go for it. That's the way to do it. Um, Mal, husband and I make 375 and are still living monthto-month. Now, that's a tough one because that's really going to come down to a lot of behavioral finance questions. How did we get here? What's driving it? What uncomfortable choices are you not wanting to make? How are we here? Because you're crushing it financially. So, I always say look at your big three, right? So, you got your housing, your transportation, sometimes education, and I would also venture at your income level, vacations, um, things like that. And you just got to make choices that I think we have 90 people here right now. 87 of them are going to be like, WTF, cut that. It's going to be uncomfortable for you, though. So, you need to just start having those tough conversations because it's all psychology at that point in time. The math is the math, but there's going to be uncomfortable choices of downsizing housing, downsizing vehicles, uh not taking vacations, um and then maybe looking at children's education, too. Are you in an expensive private school? Do you not need to be? Things like that. Uh I need to get student loans, but everyone is worried about being a co-signer. What could I say? Oalihyah, they are all 100% justified in being afraid to be a co-signer. Um, with that being said, you need to borrow your federal student loans first and then you need to find a cheaper school. Like that's it. Mell says, "Can I list those three again? I don't even know what they were at this point in time. " Um, Tom Collins, you can consolidate a single parent plus loan. I have a parent plus loan and I'm a teacher. Track 780 says, "If I'm a parent plus loan and a teacher, will I be eligible for PSLF? " And the answer is, if you've consolidated said parent plus loan and you are on an income driven repayment plan, yes. If you have not consolidated the parent plus loan, the answer is no. Currently in forbearance with only five payments left to meet 120 310, you should have come out of forbbearance last year when I was yelling at you. So yes, you have zero financial benefit from remaining in forbearance at this point in time because whatever buyback you're buying back at is the same five payments. And I would actually worry that you are going to pay five payments that are more expensive today in 2026 than you would have paid even 2 months ago. So yes, 3M1010, you got to make five payments. And so I think this is the one thing that a lot of people are missing from this conversation is that yeah, it's really nice to have a $0 payment and if you're going for forgiveness, who cares that interest is growing, but at the end of the day, you have a set number of payments. In this case, it's five. And your goal is to just make the five cheapest payments that you possibly can by law. And so for his situation or her situation, I venture $100. those cheapest payments would have been last year. And so fast forward to today in 2026, we're going to make probably slightly more expensive. It's not going to be detrimental, but you cost yourself a little bit of money by waiting. Granted, it felt good, but you just got to make the five payments. Uh they will increase the student loan borrowing power if you get denied a parent plus loan. They do let you have the independent student limits if you are denied, but it's also discretionary and the school does not have to do it. 90% of them will do it though. Um Katie, if I'm married and we actually live in separate houses, if I fill out the FAFSA for my daughter, um does it go by both your incomes or just mine? Uh it will go by both your incomes. If you are in the process of a divorce or separation, you would have to appeal that after the fact, Katie. All right, guys. Chris RN20 2017 says, "I'm seeking PSLF. 24 months left. What repayment plan should I choose? " Chris, you got IBR, you got pay as you earn, you got the WAP plan this summer. Your goal, like I just kind of ranted on, is to figure out whichever of those three is the cheapest for you. And you do that for 24 months. That's the only goal with PSLF, guys. Lowest qualifying monthly payment. No other like thinking is required. Uh Lindsay, you go on to Lindsay asked, "How do I know if I'm in deferment or forbearance? " So, you log into studentaid. gov and you click on my aid. You click on your loans and then you it drops down and it'll tell you your repayment status. So, you wanted to say in repayment, not in deferment or forbearance. Bri says, "Can you talk about alternative income documentation? I'm going on disability soon. Um, and I want to use those small checks. " It's a great thing to do. So, when you go on studentaid. gov and it asks you like on the very first screen it says like, "Do you want to link your tax return? " you scroll past that and at the bottom you say like skip it and then you say I want to upload alternative documentation and then you can upload I always say like put a little letter on there and say like I'm currently on disability my only income is this and you can have like a little copy of it and then there you go and then you just upload that paper show your disability check and you rock and roll if you're unemployed similar process I'm unemployed here's my unemployment compensation that's all my income right now boom done. Miss Mary, you need to be on IBR today. That's it. Um, Jay, my daughter is going into her freshman year of college in August. Can I appeal my daughter's FAFSA? Jay, you can absolutely appeal your daughter's FAFSA. If you have already accepted admission, you're not going to get any more merit aid. If you uh have a change of financial circumstances or something like that, they might get you more need-based aid. Um but a big part of accepting enrollment is also accepting the price tag. So, um I thankfully because of you consolidated my loans back in March. How long before I hear back, Jaylin? Uh, it's taking 30 to 60 days. So, you only did it in March 29th. I bet you might hear something by the end of the month or early in May. Uh, even if we don't need to take out loans for a child, should we and hope they are deferred? Absolutely not, user. Don't borrow debt

Using Alternative Documentation for Job Loss or Income Drops

you don't need. Uh, daughter having to apply for disability, cosigned student loans, trying to retire. Any options? Um, mama is she? It's a very tough place to be in. For the private student loans, there are a couple lenders that do offer some types of disability options. So, check with your lender. I would also make sure that your daughter's disability is approved. She's on SSDI and you can show it. Um, otherwise, you're on the hook for that. Uh Sharia says, "I have student loans from 2019. I didn't get my full curriculum and can I get this off? " Sadly, probably not. So, Sharia, if your school closed, you could do closed school discharge if your credits that you did take can't transfer to another college. Number two is if you were defrauded by the college and that's why whatever happened happened, you can apply for borrower defense to repayment. However, most of those don't get approved because most people can't prove that they were defrauded and things have changed a lot since the lawsuits that we're seeing people get forgiveness for. With that being said, not finishing college is the roughest place to be because you don't get the benefits of the degree, but you still have the debt. So Shariah, for you, make sure that you are not just ignoring it because collections will be starting. So you need to make sure that you're getting on an income driven repayment plan while you navigate these options and uh make sure it reflects your income today. Rich said, "I finished paying off my student loans. Did I make a mistake? " Absolutely not, Rich. Uh again, I've been doing this for almost 20 years, and I've never met anyone that's actually regretted paying off their student loans. Uh, could you have been maybe been more optimal about it? Sure. But at the same time, like no one's perfect all the time at every financial step. So, you're fine. Congrats. That that's a big one. All right, guys. We are rocking and rolling here. I haven't seen some hearts in a while. So, please like, subscribe, make sure you're following us. Tap that screen. I'm going to keep going through your questions here. I see a bunch of them. I love it. If you guys want to come up and ask, thanks, Alexandra. I appreciate that. Uh, request an invite to speak. I can bring you up on stage as well to talk. Um, Kristen says, Kristen, do you recommend taking federal loans even if you have money in the 529 plan? So, the order of operations that I recommend is pay your known first. Always pay your known loans. So, drain the 529 plan fully and then supplement. The reason is one-third of students that start college don't finish college. You don't want to have leftover money in your 529 plan. You don't want to borrow, have the debt, and then have this extra money because not every state let you use your 529 plan to repay student loans. So, use the 529 plan upfront. Part two is borrowing can get easier in later years. So, your federal borrowing limit goes up a little bit every single year. Part two is there are no co-signer student loan options available for private loans, but those are only typically available to juniors and seniors at specific colleges in certain majors. Because the only reason these lenders are even offering no co-signer private student loans is because they're using data. And the data says that seniors specifically and some juniors in certain programs have a high graduation rate and a high income rate. and they're basing your underwriting on the data. So, if you have cash, use the cash up front and then you have more options later on to borrow, but you're also hedging that downside risk that your child does become one of the onethird of college graduates that are college students that don't finish. Uh Jamie, my save plan, my save payment was 750. I don't think with my income I can get any forgiveness. Probably not because if your save plan payment was $750, your IBR payment is going to be $1,500 maybe and your RAP about the same. You're going to pay off your student loans, Jamie. So, you're in one of those situations where if you're not one of the 50% of borrowers that's getting loan forgiveness cuz your financial circumstances have improved to such a point where that's just not going to happen, then you just need to start focusing on something like a debt snowball, debt avalanche, and just pass just get rid of that debt fast as you can. Uh, I'm going to make around 110 10k this year with 26K in student loan debt. ATX13, that is awesome. you're not going to get any kind of forgiveness because you're going to pay it off well before then. So, just execute and get those debts done. They won't deny you, Jay. Vasquez, it's just going to be such a high amount. You're going to pay off your debt. Um, what if we are watching for rap to get out of save waiting for rap? That's a fine plan. As long as you've run the numbers and you have the plan, Caitlyn, I'm not going to stand in your way of that. That's a it's a totally fine plan. XO Eva Jane says, "Is it true that you can get forgiveness for loans? " Like I said, there are over 80 different programs XO Eva Jane. However, none of them are do nothing and get forgiveness. All of them require work, time, and money. And so, the best ones are teacher loan forgiveness. Go be a teacher for 5 years, and they'll give you 5,000 or 17,500 depending on what kind of teacher you are. Public service loan forgiveness. Uh over 150,000 people are going to get their loans forgiven under PSLF this year, but it requires you to work in public service for 10 years. Make 10 years of qualifying payments and any remaining balance is forgiven. What's public service? Federal, state, local government, teachers, firefighters, public health. Uh and it's not just the teachers. It's like working for the school district. You could be an administrator. You could be uh a maintenance person. just got to work for them. Uh what else are some other big categories of it? I think that's most of it, but there's so many options for public service loan forgiveness. Um and you just have to be employed by one of those eligible employers. You also have timebased loan forgiveness exeagane. So if you're on IBR, it's 20 or 25 years. So if you keep making your payments along for 20 or 25 years and you still have a balance, it's forgiven. The repayment assistance plan is 30 years. You got total and permanent disability. happens, you get totally disabled, forgiven. Then you have all the state programs, XO Eva Jane. Uh there's so many of them, but some of my favorites are Maryland has a home buyer program. You buy a house in Maryland, uh they like roll your student loans into your loans, forgive it, and give you credits on your mortgage. Kansas, same deal. Maine, you go become an engineer or work in a STEM field in Maine, and they give you money towards your student loans every year. And there's just more and more of these programs popping up. So, completely lots of ways to get student loan forgiveness. XO EBA Jane. Oh, and I didn't even talk about all the employers that are doing it these days. Uh, this new survey came out. It's like 18% of the Fortune 500 right now is offering uh up to 5250 in student loan repayment assistance. So, you go work for one of these large companies, you get 5,000 bucks a year to your student loans. There's just a lot of options, but again, they all require you to do something. work time, pay your loan payments for a certain period of time, all the things. So, follow up. Eva Jane says, "I'm in Oregon. I'm not able to work. I have 400 canculed loans. " So, again, income driven repayment. That's fine. Hey, you know, it totally happens. Get on income driven repayment plan. If you have no income, your payment will be $0 a month. If you have no income, most people still have some income, so it might not always be zero. And you just keep riding that thing to the sunset to the point where you're either totally disabled and you can get them forgiven for total impermanent disability or you get timebased loan forgiveness because you've had a $0 payment and you just keep riding those things into the

Should You Empty a 529 Plan Before Taking Out Loans?

sunset. Leavonne, if you are actually going to pay off your student loans before the forbearance is done, yes, go for it. Now, I'll tell you, the behavioral psychologist in me says that you're more likely to actually succeed if you enroll in repayment, but I'm not going to on what's working. If you are doing it, keep it going. All right. Olivivera says, "With parent plus loans being capped at 20K, what are the best options for additional funds if needed? " Well, my first thing is please don't go to a school that's going to require you to have additional funds between the child and you. You guys can borrow $92,000 together. If you are borrowing that much for a bachelor's degree, you are hurting yourself and your child financially for 20 years. So, it's not worth it. You can always take a private loan. I'm not your mom. I'm not going to gatekeep how to do it, but it's a very very bad financial idea to do it. If you didn't see my video from like two days ago on the break even, uh that's based on $80,000 of borrowing. Takes you to 34 to break even. You're going to go up to 92 or even more. I mean, your child's not going to break even on that educational debt until they're 40. And it's like at that point in time, that's just catching up to the high school folks. So, it's like you didn't even need anything. You just did. So, Olivivera, please just don't do that. Go to a cheaper school. Um Melissa, I'm currently on save. I'm starting my masters. Apply for FAFSA. Um do I choose a plan this summer? Uh so, depending on how all the timing is going to line up on your loans going back into inschool deferment, the answer is maybe. Um, I don't know exactly how they're going to line you up on that one. Uh, there's a good chance that you might just roll right into inschool deferment status and you're not going to have to choose anything until after that. 95% chance that'll happen, but there is a scenario where things get botched. So, you just need to watch it and make sure that your loans do end up going back on in school deferment. All right, guys. Um, nope. And not today. Okay. What loan would you recommend for a student that hasn't had any loans and would need to borrow about 12 to $15,000? All right. Nope. And not today. Remember, federally, you as the student can only borrow 5,500 freshman, 6,500 sophomore, 7500 junior, senior. Beyond that, you're going to have to supplement and you're probably going to need someone involved, parent or a relative that's going to cosign, but a parent can borrow a parent plus loan up to $20,000. Like we just saw that other commenter. Uh, and then you can also cosign private loans starting in July. They're basically equal. Whichever one gives you the lowest interest rate is the one you want to go with. There's no real benefit now to parent plus loans. Um, unless they give you a better interest rate than what you'd qualify for with private loans. Danny, is it a good idea to consolidate? Uh, Danny, the only people that need to consolidate their student loans are parent plus loan borrowers that are trying to access IBR before the changes. And if you're in default, nobody else needs to consolidate their student loans. And in fact, consolidation can hurt you. And I really hope they get rid of the option on studentaid. gov of in July because it hurts more people than it helps. Um, Ethan, 19-year-old trying to buy a $21,000 car. What percent should I put down? Ethan, do you want the real answer? The real answer is you put down 100% and you buy the car for cash and if you can't afford a $21,000 car, you go find a $5 to $7,000 car and then you put down as much as you humanly can. um and you finance as little as possible. Cars just lose value. They are just to get you from point A to point B. And you're 19 years old. You need that money to work for you. You don't want to be giving your money away to other people. Ash says, "Wait for cheap community college or loans for uni. 2 years bachelor's of nursing, 70kish of debt. I'm not quite sure I understand your question on why you're waiting and what that looks like. Uh Cheryl says, "Isr based on both incomes for married couples? " Yes. And if you're both married, I got to make a video. I'm going to take a note to make this video on this one tomorrow before I forget because uh you guys ask this all the time and I just need to draw it out for you. But one second. Married with loans. All right. So, you're married with loans. You both have loans. You're going to calculate your payment as married filing jointly, whatever it is. I'm going to call it I'm going to make this really an easy example. Let's say that your monthly payment is $1,000 a month using WP or IBR and you each have $50,000 in loans. So, it's like 5050. So, what it does is your overall payment as a unit will be a,000 and each of you guys would have a $500 a month student loan payment. So, what it does is it kind of divides out proportionally to your debt so that your overall debt is the same payment. And I really did a bad job on that. So, that's why I want to explain this in a video, but that's how it works. If you're both have student loans and you're both on an income driven repayment plan. Uh Koko, I'm in PSL. I have 69 payments that count. Uh do I have to be in an IDR plan? Uh Koko, you do. You need to be in IBR, pay as you earn, ICR, or the upcoming WAP plan? That's where you need to be. You should already be there because you're just costing yourself time and money. So, if you're not an IBR yet, today's a great day to go on studentaid. gov and enroll. Jessica, do I still qualify for PSLF? I'm an hourly employee. Absolutely. It doesn't matter as long as you're 30 hours a week or more because that's full-time. So, you got to be 30 hours a week or more. Um, and qualifying employer, qualifying repayment plan. Lindsay says, "Do you have to work at PSLF for the 10 years when making the payments or just the time of application for all 10 years? " So Lindsay, they actually treat every one of the 120 payments is individual. Every single one. And you have to meet all the criteria for each of the individual payments. Direct loan, qualifying repayment plan, um qualifying employment, and then you certify it all, every single one. And granted, most people certify every year, and it just like knocks out all the 12 payments before that. Leslie, how much would the monthly payment be for a uh $20,000 parent plus loan? So, Leslie, I don't know if you're asking for the new system or the old system. Oh, man. I touched the screen and now I lost Oh, there you are, Leslie. I got you back here. All right. Standard re. I'm gonna do it right now because we are sitting here and we we're capable of doing hard things here. Leslie, I'm going to pull this up here. So, you have $20,000 balance 9%. Your payment is going to be $253 on that $20,000 uh parent plus loan. And that's using the new tiered standard plan that goes into effect. If you get on an income driven repayment plan, it will be based on your income. So, Nita JB19 says, "I don't know what to do. I have Moila. I owe 30K. What plan should I go on? " So, Nita, you have a couple options. You have the standard repayment plan. If you're trying to pay off your loans, that's the one that pays off your loans. If you're looking for the cheapest monthly payment and or you're going for loan forgiveness, you got IBR, you got pay as you earn, and you got the upcoming WAP plan. The answer to your question is going to be go to our calculators, run the numbers for your situation so that you can know your repayment plan options and then you just go apply for it. Deborah, that is rough. That means you borrowed quite a bit of money. Zper me ZP MS 10 says, "Any PSLF buyback news? My request has been escalated for 17 months. " Uh you can see the latest today the backlog is down to 27 months but ZP MS what we talked about at the beginning of this show is that I think that 50 to 70% of that backlog is going to get cleared out through denials and they're denying it because everyone's going to have to hop on a repayment plan and you're going to finish PSLF the normal way probably before your buyback is processed. Now granted, since you have 17 months, you're probably only trying to buy back like 3 or 4 months. You might still have hope, maybe, but anyone trying to apply for buyback in 2026, there's no hope. Just get PSLF done the normal way. Um, congratulation nation says student loans are ridiculous. Uh, I would tell you that yes, student loans are the most complex uh consumer financial product that exists. Um, Brooklyn girl says, "If the parent is a teacher, does it apply for a parent plus loan? " So, teachers that currently have a parent plus loan can consolidate, get on income driven repayment, and qualify for public service loan forgiveness. New parent plus loan borrowers after July 1st will not have access to public service loan forgiveness simply because they don't have access to an income driven repayment plan. All right, Miss Annie says, "Do payments made while in school deferment count towards PSLF? " No, they do not, Annie. And you bring up a great reminder. So, you guys might have heard me say this many times before. Do not make payments when you're in deferment or forbearance. Do not make interest payments when

Do In-School Deferment Payments Count Toward PSLF?

you're in school. Most people end up costing themselves money that could be going to other things. If you feel like you got extra money when you're in college and you want to do something with it, invest it. That will go a whole lot farther than paying off the interest because remember about 50% of all federal student loan borrowers qualify for forgiveness. Plus, we have all the state-based programs. employer programs. Don't pay interest while you're in school. Don't payments when you're in deferment or forbearance because that all is just wasting money more often than not. Deborah says, "Should I file for bankruptcy? I can't pay off my private loans and my husband also has them. " Deborah has a very tough spot to be in. I highly recommend you go talk to our friend Jay, the student loan lawyer. You probably seen him on this platform. His specialty is bankruptcy and student loan debt. That's what he does for a living. Go check out his videos. I know him in real life. He is a real lawyer and uh this is what he does. All right, guys. Uh Diana says, "Does it make sense to go back to college at 63? " Uh Diana, if you can afford it or it doesn't cost you anything, go for it. Enjoy lifelong learning. If you cannot afford it, the answer is no, it doesn't because you want to retire and you don't want to have a financial burden over you and your family for the rest of your life. Uh, Aransa says, "Do you recommend consolidating five separate student loans accumulating up to 55K if I want to do R? " So, Art, if these are just your undergraduate loans or graduate school loans, you don't have to consolidate to enroll in an income driven repayment plan. You just The only people that need to consolidate are parent plus loan borrowers. And you need to do that today or else you're never going to have that option again. or if you're in default and you want to get out of student loan faster than rehabilitation. Those are the only two people that need to consolidate. No one else does. So D says, "Can I get some kind of loan forgiveness if two of my four loans is my parents' names and my dad's disabled? " So D, it's really important to frame the conversation properly. If your dad has a parent plus loan in his name, it's his loan. And if he is totally and permanently disabled, that qualifies for total impermanent disability discharge. And you can get the parent plus loan forgiven. Parent plus loans are the parents loans. The child has no legal obligation to them, but you can definitely help your dad get the forgiveness he deserves. All right. Uh, I think we're catching up on this. So, Riley Rue, got accepted to MIT, but it's really expensive and the only way I can afford it is to take a key. I don't know what that means. Uh, but take a student loan. I would talk to your parents and figure out why because either your parents have money so you didn't qualify for enough financial aid package or uh you can appeal to the school if there was something off with the FAFSA and the CSS profile that you filled out. Chrissy, if I move from save tor or standard repayment, will my payment history be calculated been paying since 2013? Uh so with that being said, yes, you don't want to move to standard Christie. If you're in save, you just move to IBR and your prior income driven repayment will be like the number of them will be added to your IBR plan. The reason I want to say is you don't move to standard is because that's also taken into consideration and so your standard payment is going to be a fortune, right? Because it says you're already going to be done. Um, all right. Uh, Monarch Mama, how much do we think a bachelor's degree will cost in 8 years in the state? Uh, Monarch, most prices go up 3 to 8% a year. Oh, thank you, Liberty. With that being said, the average discounting now is 50%. So, I just hate the way colleges price things. Don't look at stickers so much, Monarch. I don't know how much money you have. Like, here's the thing. If you got a million dollars in the bank and you make over $150,000 a year, look at sticker prices. If that doesn't apply to you, then realize that sticker prices also don't apply to you and you should look for colleges that have generous financial aid policies and things like that. Um Jim says, "I've just been ignoring my parent plus loans because there's so much. What am I supposed to do? " So Jim, you gota I don't know where you stand, but you got to consolidate them and get on an income driven repayment plan and you need to do it today because that window to consolidate and get on an income driven repayment plan closes in June 30th and consolidation can take 60 to 90 days. So, Jim, consolidate income driven repayment. That will be cheaper than the collections that will come for you because remember guys, if you don't pay your loans, they're going to garnish your wages at 15%. Or if you're old, they're going to take 15% of your social security. They'll disability. Uh they can take state tax returns, federal tax returns. It will be more costly to not pay them than to get on an income driven repayment plan. But that window closes, Jim. So if you have not consolidated and got on an income during repayment plan, uh do it. Uh sin is Colombia University worth it as a transfer student? It's very hard for me to judge worth it. Um and what I mean by that is it worth it financially? uh if you want to buy it and you have the money to buy that school, buy whatever you want to buy. But if you're taking on student loan debt for that experience, the answer is bar none, no. Financially, it is not worth it. However, it's kind of like asking me what car should I buy? Should I buy a Ferrari or Honda Civic? Right? Both of them get me from point A to point B. Both of them are fine vehicles. If I have the money to buy one and a preference to buy one, you can buy that one. But if you're borrowing and you don't have the money, well then buy the one that you can afford because it does the exact same thing. I don't know if you were here for my conversation earlier, but I just came out of a higher education conference. We had the Gallup people there. Those are the guys that do all the polls in the news. And uh they did an interesting study where they asked employers, do you care where their your employees went to college? And no, none of them care where you went to college. They waited it exactly the same. Um, and I can say that from the workplace. I want to get one of our HR friends on there. She's the chief HR of a Fortune 500 company and literally will tell you the same thing. Um, SVPO, two kids just graduated, 40 and 50K, no work yet deferment. SVPO, uh, whose loans are they? Because the kid can't have 40 or 50K. they can only have 28K. So, if there's parent plus loans involved or private loans, you don't want to keep deferring them. Especially if you're on the hook for it, you need to step in and pay your own loans. They can get on an income driven repayment plan for their federal loans and have a zero payment. So, it's really a question of whose loans, what kinds of loans, all the things. Uh, Exo Eva Jane says, "Can you explain deferment forbearance and should I take them out of that? " Yes, because you have no income. So, deferment and forbearance allows you to not make payments on your student loans. It sounds great, but time spent in deferment or forbbearance also doesn't count towards forgiveness. And for you, Eva Jane, that you are disabled, you want your time to count for forgiveness. So, if you have no income, you can apply for an income driven repayment plan with your no income and your payment will also be very low or $0 a month. But the benefit there is that low or 0 a month payment counts for loan forgiveness. So, you start making forward progress to get those loans wiped out. And that's what you want. You don't want to just leave them in deferment or forbearance because they're just going to keep growing and not making any progress. And you're just delaying time for the same exact monthly nugget. Emily, haven't looked mine in 20 years. Studentaid. gov. Log in. Check it out. Karen, two payments away from nursing uh student loan forgiveness. Congrats. I love seeing that. KZ Char says, "Married filing separately. Will they use my spouse's income for repayment? " No, they will just use your income for repayment. KZ Chart, it's important to note too that if you have children, dependents, uh, and you want to apply for the WAP plan, they have to be on your return. They will use the same, um, dependents that are on your, um, tax return, too. So, if you file separately, make sure you split the kids up correctly. Um, no. I plan to go to law school four years from now. Should I do the 22 method? Uh, no. Yeah. The cheapest way you can get there is always going to be the best way. Ash says, "Come is cheap, but it could take me years to get in. Accepted to uni, but we'll need loans. " Uh, nursing is still one of the best majors for ROI. There is still a large ROI there. It's not the worst thing, Ash. Um I don't know where community college is that impacted. I'm kind of shocked by that. I'd love to see where that is. Um but it's not a bad thing. You're just going to have to weigh the cost benefit. What do nurses make in your community? Um and all that kind of stuff. All right, hold on. Let's fix our Tik Tok here. All right. Are we back? Maybe. Maybe not. Come on. Where's my Oh, man. There we are. I don't know why Tik Tok did that. Good old Tik Tok. Let's get this repositioned in here. There we go. Oh, get that back there. Sorry guys, Tik Tok was freaking out on me. We are back in action, though. You guys can see I'm in the office here doing the thing. All right, we are almost back here. There we go. We'll do that silly Tik Tok. All right. Sorry, guys. Let me get back to the questions. All right. Um, Millennium Ohio says, "My loans were with Ascendium before a default. Are those personal loans? " No, they're not. They are federal federally backed FFVL loans. So, you just need to get them consolidated or rehabilitated and back on track. Millennial in Ohio. Um, American Sparrow, I was told to just wait. Only need 6 months for buyback. Honestly, I don't know if you're going to be able to American Sparrow. I mean, you can keep waiting, but they're going to make you choose a repayment plan and you might finish PSLF the old fashioned way before you get your buyback. So, you're risking it. I hate seeing that because if we were having this conversation in this month last year, I would have said I would have begged you with all my heart to get on IBR and get

FAFSA Appeals & Negotiating Financial Aid

done. You would have gotten done. It would have been the same price. Now the price might be a little different. Um but I don't know, you might pay more. You're already committed though to waiting. Sabone, I was fully forgiven for public service. Thank goodness. 210K. Congratulations. That is awesome. I always love seeing that. I don't know if we can get the sound effects going. Oh, yeah, we can. All right. What happened is I did chapter 13 bankruptcy to my spouse. Um, yeah, Deborah, you got to talk to a bankruptcy lawyer for that one. Uh, FA is only covering 1K of my 20k grad school. What's the best private loan? So, Sid, there's no best. We have a list right here. The best one is going to be the one that offers you the lowest interest rates. So, go shop and compare and get three to five quotes and then whoever gives you the lowest interest rates the one that you want to go with. Um, Logan, is it normal to reapply for R plan to uh to loss of hourly rate? They put my loans in forbearance. Uh, you did the right thing. If you your hours drop and your pay drops, you want to reertify your income. I'm venturing that you're in a processing forbearance, not like an actual forbearance, unless you called them and asked them to be put in forbearance and not just did it online. So, go from there. Janet, I didn't see your question, so drop it in again or I'm not there yet because I'm scrolling through a lot of questions. I just received an email saying I need to switch. Yeah, knowledge. I don't know if you watched my video from this afternoon, but again, I don't know how much you're trying to buy back when you put your buyback application in. Uh, if in 2024, I think you'll be okay to keep waiting. If you put your buyback application in anytime after about March of 2025, they're not going to process it. You're going to have to choose a repayment plan, and you're going to finish PSLF the normal way, well before they process your buyback. S5 or SS. Is 4. 95 a good percent for a used car loan? It is a good percentage for a used car loan, but like Lord help us. Stop with the car debt, man. The car debt's killing Americans. Um, oh, American Sparrow. I was told to wait till buyback is decided. I only need six months. Again, if you applied in 2024, I think it's safe to keep waiting. If you applied in 2025, I don't think they're going to process your buyback before you're forced to make repayment plan choices. So, D, I think that's an AI myth. There's no issues there. Uh, do payments with made in administrative forbearance while waiting? No. Don't make guys don't make payments while in deferment or forbearance. So, Yoli, no. And you can't get a refund for it. You just literally lit money on fire. Don't do that. Uh, Logan, I made a payment. They I put my loans in forbearance while I reapplied. Yeah. So, it's a processing forbearance. It'll be done in like 30 days. It's not even going to take that long, but you it could take you up to 60 if the your lender or your lender your loan serer starts with an M. Um, Opera, congrats. Nice to get it done. Uh, PST 1995, uh, once you get 250k in money market, should you open a second money market to get the account insured? Uh, PST, I think there's value in diversifying that, but I actually have a bigger question. is what the hell do you have so much cash in a money market for? Uh, you know, there really are there is really a risk to that and the risk is cash drag in that you are potentially costing yourself tens if not hundreds of thousands of dollars, maybe millions of dollars u by keeping so much cash versus keeping it invested. Now, maybe you have a purpose, maybe you're trying to buy something or whatnot. Uh, but damn, that's a lot of cash. I would also look at optimizing that much cash if you're looking for something to diversify your portfolio on a risk-free basis. Uh rolling treasuries, municipal bonds, other safe cash derivative products that might be more tax friendly, still give you the safety you're looking for. Um but that's a lot of cash, man. I hope you're telling me that in the context of you got a $10 million portfolio because like that that's just that's so much wasted money, man. Oh. Uh can you explain loan consolidation for parent plus loans? So parent plus loans, the only way a parent plus loan can access income driven repayment is to consolidate. That goes away on June 30th though. So you need to consolidate today if you want to have that option. ABA Jane uh May for a college student which is the best student financial or personal don't know what you're asking. Uh Tina I disabled and I applied for discharge and was denied. What can I do? Tina, I think context here is important. So why were you denied? Uh I'm guessing it wasn't a service connected disability because that's all in the VA database. If you are trying to get a doctor's note, I'm guessing, and you're not on SSDI already, the key is get on SSDI with at least a 5year review period. That's what's required to get your disability discharge. Um, so I don't know why you were denied or what the whole background is, but that's what you need to know. Uh, Emma, how are monthly payments calculated for borrowers who are filing married filing separately? Well, it just uses your adjusted gross income from your individual tax return. Uh, don't speak says, explain parent plus loan consolidation and why. So, don't speak. If you need access to income driven repayment and public service loan forgiveness, you need to consolidate today. like literally today because June 30th that closes and starting July 1st, parent plus loans that are not consolidated can never access income driven repayment and public service loan forgiveness. You will only be able to repay new parent plus loans and non-conolidated parent plus loans on the standard plan. Also, when you say you only each have one, it also means you can never borrow again. So, I don't know where you're at with your kids in school, but you can't borrow a federal loan again either if you need to have access to those. Uh Lana says, "How can my daughter refinance a non-federal loan into a uh that is a variable rate to a fixed rate? " So, Lana, go shop and compare. Go tell her to go online and shop and compare uh and find a new student loan. I will say that variable rate loans have typically won over the last while because rates keep dropping. Um but I get it. You want to lock in a rate makes it a little more um makes you feel a little more stable. AJM add or AJ Maddox. Maybe I should read the whole thing. Why does interest acrue so quickly while on IBR? Well, AJ, uh, the big thing that you need to realize is that when you're on IBR, your monthly payment is based on your income. It's not based on your loan balance, your interest rate, anything like that. Most people are on IBR because they want the lowest payment because they're going for some type of loan forgiveness, right? Or like financially, you can't afford the standard plan payment. I guess the big thing I should say is if you are looking to repay your student loans, the standard plans are what repay your student loans. This is standard, extended, and graduated. I don't like graduated because it does that hockey stick thing. Those payments will pay fully a pay off your loan, principal and interest, and the whole shebang. Most people are on IBR though because they can't afford that. And so, no, you don't want to like pay extra on IBR because you can't afford to successfully execute the plan on standard. But what you can do is look for forgiveness programs. You could start investing that little bit of extra money in an IRA. Uh lower your adjusted gross income, put some more in your 401k to lower your adjusted gross income and lower your um your monthly payment. Because if you're like it's like one of those things the worst thing to do when it comes to student loan repayment just like college is to fail. And paying extra on your IBR payment but not getting to the standard payment is failing because your money is not making the progress it needs to make to successfully execute the plan. So you're wasting it. And I don't like people wasting their money. And so either you get on standard and repay or you stay on IBR and you keep your payment low and you invest and build wealth while maximizing it. And maybe in 5 years though you start making a lot more money because I also think people forget that time like the government's betting against you. They're betting that you're not getting forgiveness because the government knows that most people will pay off their loans in 18 to 22 years, which is before the forgiveness window. And they know this because they have access to all the IRS data and the Social Security Administration and they know exactly how much you make. And so you, most Americans, there's always the exception, but most Americans earn more. You start at 22, at 25, you get into your 30s, 35, 40, start making good money. Maybe your plan changes, AJ, but at least one, you didn't waste money. Two, you maybe started building a nice nest egg for yourself in your 401k and your IRA, and then when you get to this point where you're making more money, you can successfully execute the repayment plan and get the loans paid

Securing $0 Monthly Payments if Unemployed or Disabled