Portfolio Performed Better Than Expected In Retirement? Adjust This Now

Machine-readable: Markdown · JSON API · Site index

Описание видео

Learn more about our services at https://www.parallelwealth.com/planning

In this video, I'll go through how the recent good markets have turned into a bit of a tax problem for retirees, and how you can think about updating your plan and drawdown strategy to solve this.

If you have any questions about this video's topic or retirement planning in general, visit https://www.parallelwealth.com/ or use the links below to learn more about our services:

➡️Fee For Service Retirement Planning: https://www.parallelwealth.com/planning

➡️Retirement Income Program™: https://www.parallelwealth.com/investments

➡️Parallel Wealth Masterclass: https://www.parallelwealth.com/education

More from Parallel Wealth:

🔗https://linktr.ee/parallelwealth

The above affiliate links are provided for your convenience. If you click on a link and end up purchasing a product or service, this channel may receive compensation for the referral. We have personal vetted each product and service we provide links to.

DISCLAIMER: This presentation is for informational purposes only and should not be considered financial, investment, tax, or estate planning advice. All investments carry risk, and past performance does not guarantee future results. Any forward-looking statements are based on assumptions and may not reflect actual outcomes.

The content on this channel is for educational purposes only and does not provide specific investment or planning recommendations. Viewers should consult a qualified professional for retirement, tax, or estate planning guidance. Parallel Wealth and Adam Bornn are not responsible for any decisions made based on this content.

TIMESTAMPS:

0:00 - Intro

0:36 - Before we make any changes

2:50 - Base scenario

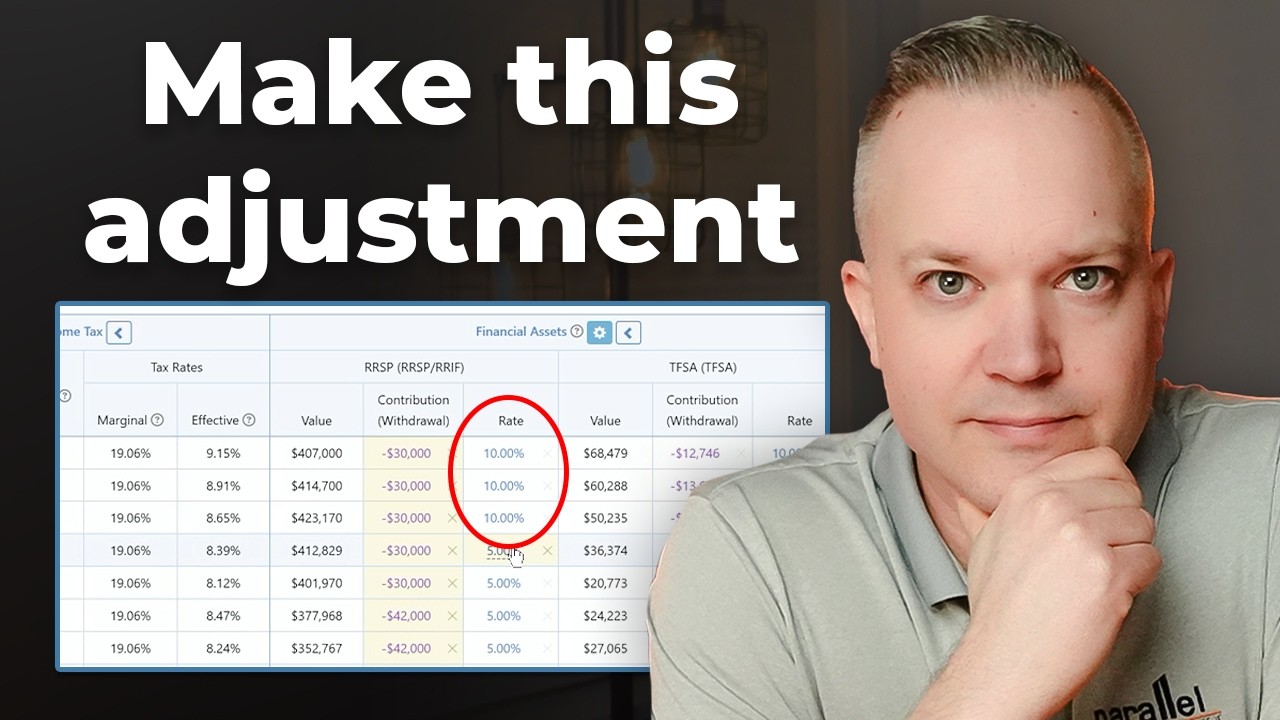

5:06 - What if they get a 10% return?

7:03 - Adjusting the RRSP meltdown

9:40 - Can they spend more?